All Categories

Featured

Table of Contents

TAKE TIME TO READ IT. Do not allow one representative or insurance provider prevent you from getting info from an additional representative or insurer which may be to your advantage.

By doing this you can be sure you are choosing that is in your benefit. We are required to alert your existing firm that you may be changing their plan. 1. If the plan protections are essentially comparable, premiums for a new plan may be greater because prices raise as your age increases.

If you borrow versus an existing plan to pay premiums on a brand-new policy, survivor benefit payable under your existing policy will be reduced by the quantity of any kind of unpaid funding, including unpaid interest. 5. Current rate of interest are not assured. Guaranteed rate of interest are usually considerably less than existing prices.

Instant Life Insurance Quotes No Medical Exam

Are premiums assured or conditional - up or down? 7. Participating plans pay dividends that may materially minimize the price of insurance policy over the life of the contract. Rewards, however, are not ensured. 8. CARE, you are prompted not to act to end, assign, or alter your existing life insurance policy coverage until after you have been issued the brand-new plan, analyzed it and have discovered it to be acceptable to you.

If you are not satisfied with it for any type of reason, you can return it to the insurance company at its home or branch office or to the agent with whom it was bought, for a full reimbursement of costs. 1161-2213I/ GA( 1206) P.O. Box 61 Waverly IA 50677-0061 Phone: 1-855-200-7101 If you have concerns or require assistance applying, please offer us a phone call.

For J.D. Power 2024 award details, see Long-term life insurance policy develops cash value that can be obtained. Plan lendings accrue rate of interest and unsettled plan lendings and interest will reduce the death advantage and cash value of the plan. The amount of cash money worth readily available will typically rely on the kind of permanent plan purchased, the quantity of insurance coverage acquired, the length of time the policy has been in force and any impressive plan finances.

Disclosures This is a general description of insurance coverage. A total declaration of insurance coverage is discovered only in the policy. For even more information on insurance coverage, expenses, limitations, and renewability, or to get coverage, call your local State Farm agent. Insurance plan and/or associated cyclists and attributes may not be offered in all states, and policy terms and problems may vary by state.

Now that you have actually figured out just how much you require, ideally the insurance business will certainly offer you that quantity. Insurance coverage firms make use of multipliers as defined above and will not give you with more insurance coverage than they believe you require, based upon their solutions. There is some flexibility there, so if you require that surpass these solutions, your representative can help you "market your instance" to the underwriter.

Instant Term Life Insurance Rates

Derek is a Licensed Financial Planner and made his Ph. D. in Personal Financial Preparation at Kansas State University. He can be reached at [e-mail safeguarded]. Find out more of Derek's write-ups right here. As the life insurance policy underwriting landscape continues to advance post-pandemic, individuals significantly have access to "instant-issue" term insurance policy choices that reduced out a number of the typical underwriting demands and seek to offer a decision just mins after submitting an application.

Initially, it may be useful to provide some definitions concerning specifically what "instant-issue" describes considering that there is some ambiguity in just how terms are utilized and that can trigger confusion. At an actually top-level, we can organize the underwriting of term insurance policy items presently on the market into 3 broad buckets: Nearly immediate decision after sending an application (less than 15 minutes).

Insurance business can customize their own underwriting policies, and we might see advancement in what is frequently needed over time. For the time being, these 3 groups do a quite good work of marking the different courses that someone might choose to go down when purchasing term life insurance policy.

After sending an application, individuals will certainly typically have choices within minutes, and the entire underwriting process is done. In order to supply instant-issue insurance coverage at practical prices and get here at a decision within minutes, service providers will certainly not have the ability to rely upon a Participating in Medical Professional Declaration (APS), medical checkup, or lab work.

For example, some providers may have limits such as $2 million for instant-issue coverage and an overall of no even more than $5 million in complete life insurance policy for an individual getting instant-issue coverage (note: these are simply example numbers). In this instance, it would be absurd to approach these providers and make an application for $3 million of instant-issue protection or for any protection for a person who currently has $5 million or more of insurance coverage active.

Instant Online Whole Life Insurance Quotes

Similarly, if a provided provider will not issue instant-issue coverage for a guaranteed with a typical cigarette ranking, after that it would not be smart to request instant-issue insurance coverage for an insured that is estimated to have a basic tobacco ranking. Moreover, it is worth keeping in mind that the threat of rejection is greater for any individual projecting at the cutoff point for an offered type of coverage.

In the last case, even if their rating does can be found in less than expected, they're likely to still be used recommended non-tobacco as opposed to rejected completely. Lastly, it is worth keeping in mind that some service providers might pick to relocate a person from an instant-issue or accelerated underwriting track to standard underwriting exclusively as an issue of arbitrarily analyzing their very own underwriting treatments and candidate pool.

Instant Life Insurance Policies

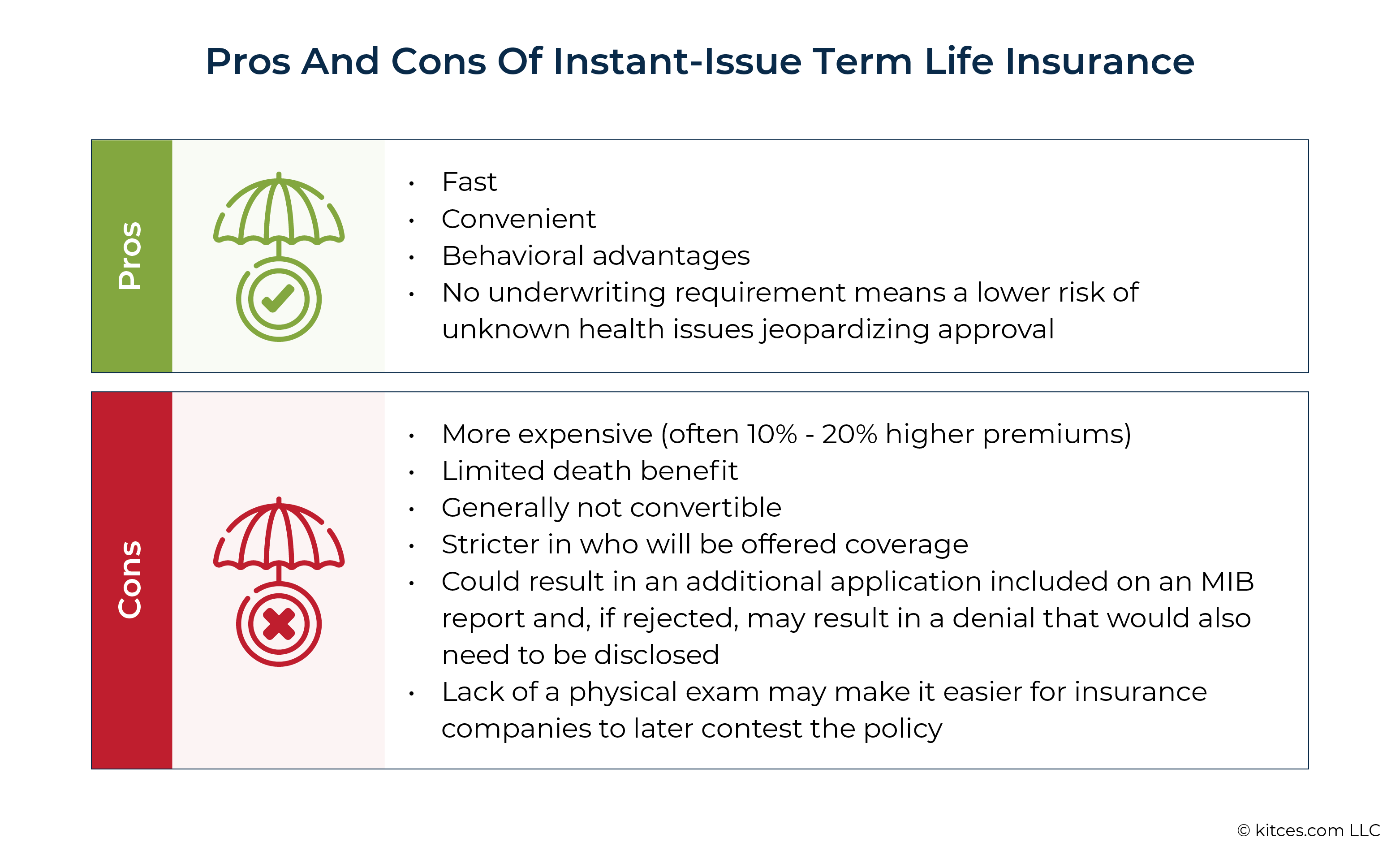

Some of the pros of instant-issue life insurance coverage are that the procedure of acquiring it is very fast and hassle-free, behavioral barriers are less likely to be a concern given that there are no underwriting requirements, and the application process is much simpler than that for various other types of coverage.

And if the application is declined, a rejection would certainly additionally require to be divulged upon getting coverage with another service provider. While the application procedure does not consist of a physical test, the absence of a physical additionally makes it simpler for a life insurance policy company to dispute a policy. Moreover, instant-issue plans normally provide a limited survivor benefit and are generally not exchangeable.

Instant Term Life Insurance Quotes Online

Depending on how quick someone can survive the insurance sets of questions, it can take just 1530 minutes to have actually approved protection in position. In the context of consultants dealing with customers and especially those dealing with collectors (in a project-based or hourly context) or much less upscale customers (that are consulted with less often) this benefit must not be underrated.

Many carriers will additionally need that EFT repayment details be given as part of the application, so also the monthly settlement can likewise be set up instantly and all set to go by the end of the meeting. Anyone who has had a hard time with obtaining customers to in fact execute life insurance policy might appreciate how big of an advantage this can be.

Working with insurance policy firm phone interviews, scheduling clinical exams, altering one's mind about protection over a 1- to 2-month waiting duration, dissatisfaction with underwriting results, and objection to reboot the underwriting procedure have actually all been obstacles I have actually personally attended carrying out term life insurance. Additionally, also for recurring customers, I have actually had customers that, in spite of my constant pestering, took years to execute coverage.

Instant Life Insurance Quotes Canada

I personally really felt that I was not meeting my fiduciary responsibility to clients by introducing barriers to executing term life insurance policy. Having the ability to offer that solution for my clients has actually reduced one set of obstacles, and the capability to supply instant-issue insurance coverage has eliminated yet another set of obstacles.

Approved, there's definitely some health benefit for a candidate to learn more about an unidentified problem during underwriting, but it is not uncommon for someone to discover something about themselves throughout the underwriting process that might make their protection far more costly, and even stop them from ever before obtaining insurance coverage. With instant-issue insurance coverage, however, a candidate only responds to inquiries concerning their health that need to be genuine as of the moment they are addressing them.

{kind=link}

Latest Posts

Company Funeral Policy

Buried Insurance

End Of Life Insurance